Increasing prices, interest rates, and economic instability are putting financial pressure on many Americans to reconsider how they allocate their spending. According to YouGov’s latest survey results, increasing financial pressure is impacting millions of American families in various ways.

In the United States, families are cutting back on non-essential and essential expenses in an attempt to cope with the increased costs of living. In some cases, individuals are tapping into their savings accounts, working additional hours, or even taking out new loans.

Key Takeaways

- Nearly half of Americans say they have reduced non-essential spending during the past year.

- A growing number of households are using savings or borrowing money to cover everyday expenses.

- Some Americans are taking extra jobs or cutting investments because of financial stress.

Americans Are Cutting Back

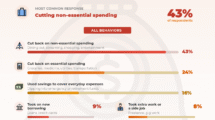

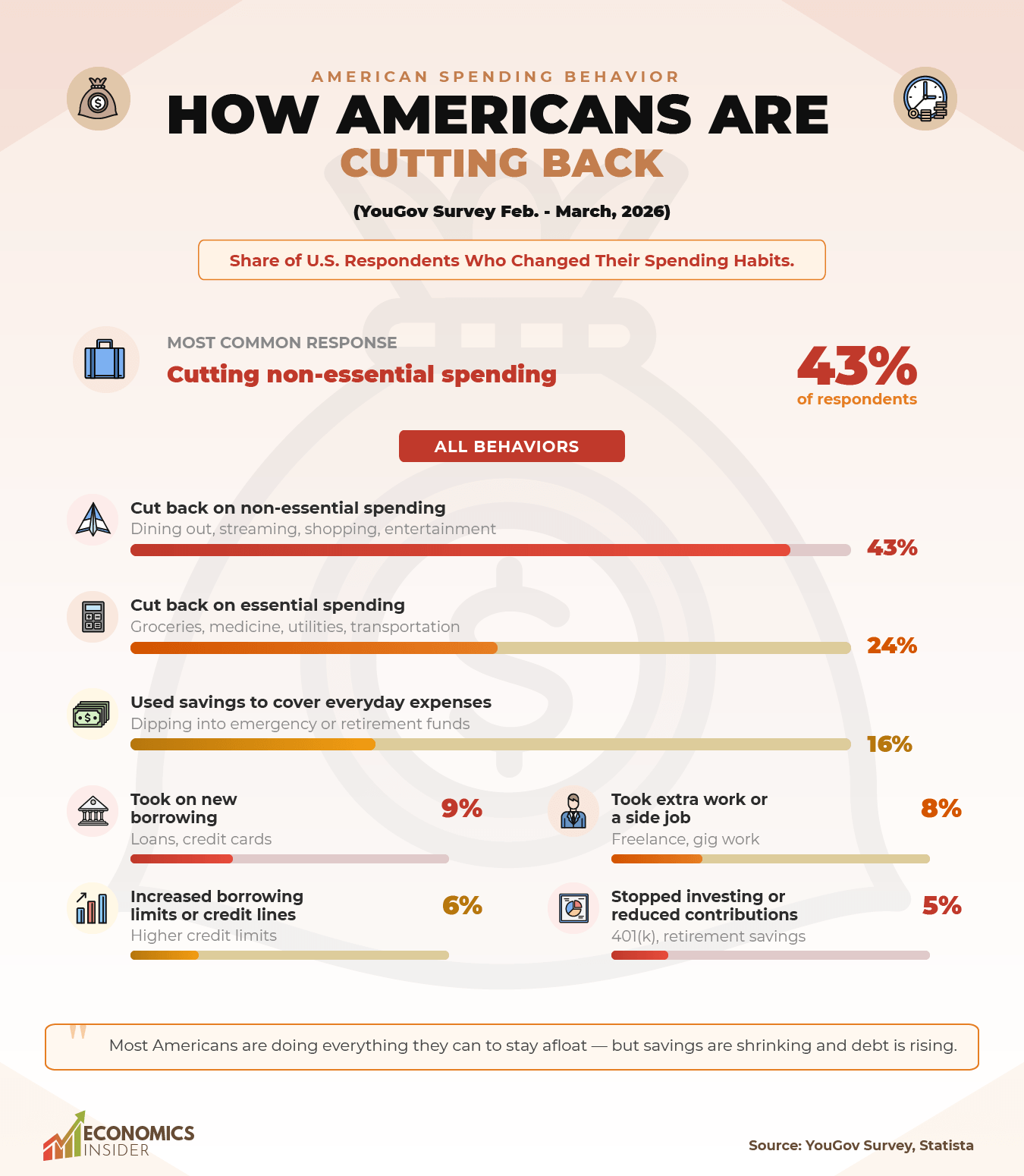

The table below shows the share of U.S. respondents who changed their spending or financial behavior during the year before the survey.

| Spending Behavior | Share of U.S. Respondents (%) |

|---|---|

| Cut back on non-essential spending | 43% |

| Cut back on essential spending | 24% |

| Used savings to cover everyday expenses | 16% |

| Took on new borrowing | 9% |

| Took on extra work or a side job | 8% |

| Increased borrowing limits or credit lines | 6% |

| Stopped investing or reduced contributions | 5% |

Source: YouGov survey of 1,450+ U.S. adults (Feb.–Mar. 2026), Statista

Cut back on non-essential spending

At 43%, cutting non-essential spending is by far the most common response. This means people are saying no to things like restaurants, Netflix, gym memberships, new clothes, and small daily treats. It is the easiest and most painless cut to make, so it makes sense that most people start here. But when almost half the country is doing this at the same time, it shows that financial pressure is very real and very widespread.

Where Americans Spend Their Money

Cut back on essential spending

One in four Americans, about 24%, say they are cutting back on essential spending. Essentials are things you cannot really go without: food, medicine, heating, transportation, and basic household bills. When people start skipping these things, it means the pressure has gone well beyond lifestyle choices. It is a real hardship.

Draining savings just to get through the month

Sixteen percent of people are dipping into their savings to pay for normal, everyday things — groceries, rent, bills. Savings are supposed to be a safety net for emergencies, not a tool for getting through Tuesday. When people have to pull from savings for routine expenses, it means their monthly income is simply not enough.

Taking on debt and picking up extra work

About 9% have taken on new debt, 6% have raised their credit limits, and 8% have picked up extra work or a side job. These are not small decisions — they all carry a real cost. Debt comes with interest. A second job costs time, energy, and health. The fact that people are going this far shows that for a meaningful slice of the population, regular budgeting adjustments are simply not enough anymore.

Quietly giving up on the future

Five percent of people have stopped investing or reduced how much they contribute to savings plans like retirement funds. This is the smallest number on the list, but it may be the most costly in the long run. When people stop investing, they are not just losing money today — they are giving up the growth that money would have made over the years or even decades.

So what does all this really mean?

These numbers paint a picture: people are doing everything they can to stay afloat. Most are starting with the things they can live without. But a large chunk of people have gone much further, cutting real needs, burning through savings, or taking on debt.